Since March 5, 2020, banks in Vietnam have been allowed to develop eKYC solutions according to Circular 16/2020/TT-NHNN – Circular guiding how to open and use payment accounts at payment service providers. So what is eKYC and why has it become a new standard in the finance and banking industry? Let’s learn about electronic customer identification with FPT.AI in the following article.

What is eKYC? eKYC vs KYC?

eKYC (electronic Know Your Customer) is a method that allows banks to verify the identity of customers online quickly, securely and accurately based on biometrics, OCR, AI, … .

Compared to KYC (Know Your Customer – a process of verifying customer identity directly at the bank counter, to ensure that the person performing the transaction is the owner and prevent fraudulent activities), eKYC shortens the verification time to 3-5 minutes, allowing customers to complete remotely via an Internet-connected device, without having to go to the counter, queue, fill out forms or wait.

eKYC technology automatically compares images, videos, and identification documents (ID card, CCCD, passport) with the database to verify identity. Currently, most banks require eKYC when opening an online account, depositing money, withdrawing money, etc., but services such as credit loans still require direct KYC.

eKYC security methods

To ensure optimal security for customers, eKYC uses a number of security methods as follows:

- Username and password: This is the basic and popular form of security today for most bank accounts. Customers can create an account and use a username and password to access and manage their accounts.

- Fingerprint or Face ID: Identity verification technology via fingerprints and facial recognition (Face ID) has become familiar to many people when logging into accounts. With eKYC, customers can set up this information security method right from the start, increasing account security.

- OTP authentication code: This is a highly secure verification method, widely applied not only in banks but also on many other platforms. OTP code (One-Time Password) helps authenticate identity quickly and securely every time you make a transaction or log in.

What technologies are integrated into the eKYC process?

OCR technology

OCR stands for Optical Character Recognition. This is a technology used to recognize characters on images/PDF files, then extract information and convert these images into text.

In eKYC, OCR helps banks identify and extract information from customers’ identification documents such as ID number, full name, date of birth, etc. to compare with available databases.

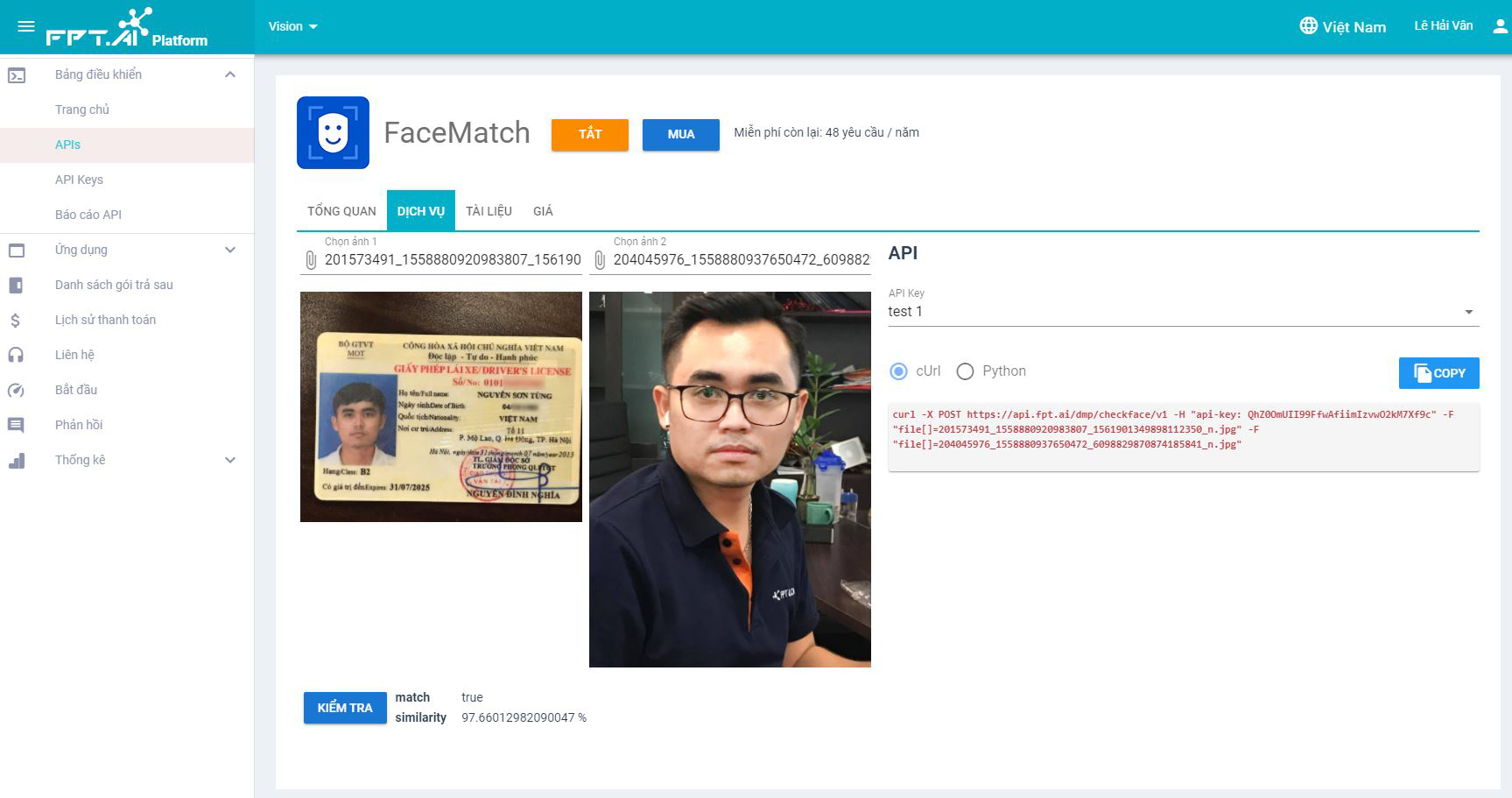

Face Matching Technology

Equipped with Deep Learning technology, Facematch AI technology can improve the accuracy of the eKYC process by analyzing and comparing the overlap of portrait photos on documents such as CCCD/CMDN, Driver’s License, Passport… with real face images/videos.

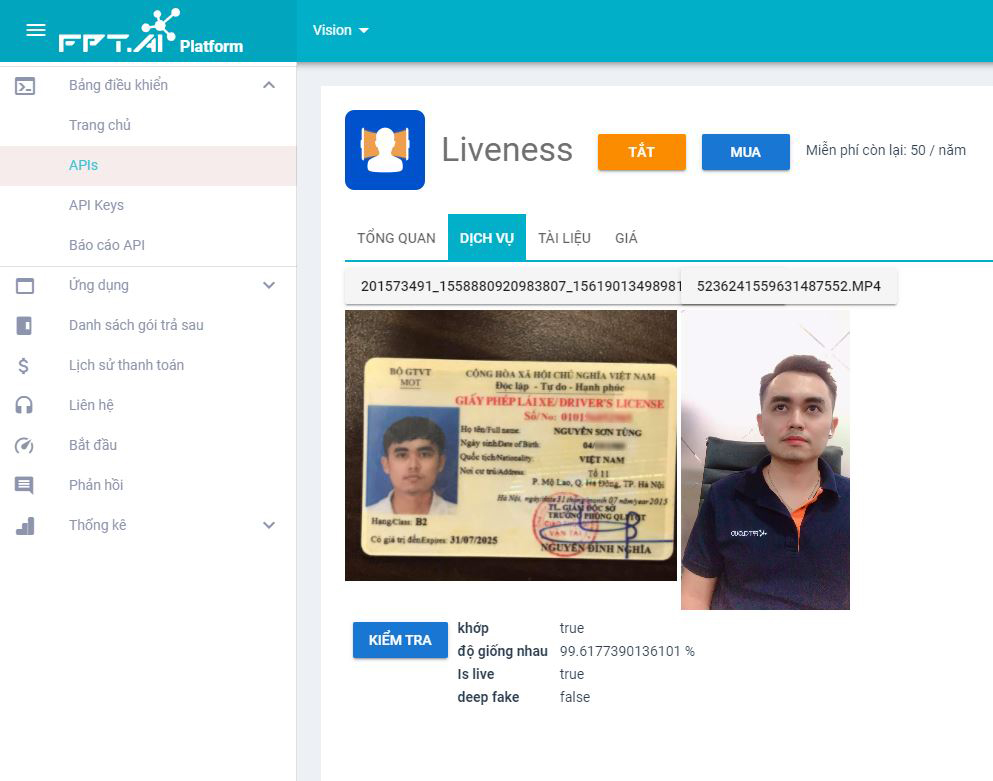

Liveness Detection Technology

The main goal of Liveness Detection is to prove that the real person (the owner) is performing the biometric verification activity. This technology is considered a level 2 defense barrier in the eKYC online identification process, helping to prevent identity theft.

Customers only need to provide 1 photo and 1 selfie video taken directly using the image of a smartphone, tablet or computer webcam. Then Liveness Check technology will analyze the data, preventing replayed videos, still images or masks.

NFC (Near Field Communication)

NFC is a short-range wireless connection that allows electronic devices or devices with chips to communicate with each other. Banks use NFC to authenticate biometrics on CCCDs, helping to improve security and convenience in the identification process.

E-Signature (Electronic Signature)

E-Signature allows customers to sign contracts and documents online when opening an account or using banking services. This technology replaces handwritten signatures, helping to verify and approve documents remotely, without time or location restrictions. This helps banks speed up transaction processing and improve user experience.

Video Call KYC

Bank staff can perform online verification, similar to direct facial recognition and verification. Compared to methods such as OTP or PIN, Video KYC is more reliable, ensuring accurate authentication of customer identity.

Fraud Detection

Fraud Detection identifies and prevents fraudulent behaviors such as using fake photos, printed photos, and composite photos to fool the identity verification system. Thanks to that, banks can minimize the risk of fraud and improve the level of security in information management and transactions.

Benefits of appplying eKYC in the banking sector

In the era of technology 4.0, eKYC has become an important solution to help banks attract customers. The specific benefits of eKYC are as follows:

Benefits of eKYC for users

eKYC helps users significantly reduce the time and effort when performing transactions, especially opening an account or bank card. Instead of having to go to the transaction counter, users can now perform these procedures right on their mobile phones, without being limited by time or space.

The eKYC process uses modern technology such as biometric authentication, AI recognition, and personal information comparison through centralized databases. For example, eKYC can compare the fingerprint sample on the ID card with the customer’s real fingerprint to accurately identify.

In addition, eKYC allows users to complete the identity verification procedure in minutes, completely online without any manual intervention. This not only saves time but also brings a convenient and efficient transaction experience.

Benefits of eKYC for banks

eKYC is an important factor in the digital transformation strategy of banks, especially in the context of banks in Vietnam competing to develop digital banking services. Using eKYC helps banks:

- Reduce costs and human resources: The electronic identification process is completely automated, data is transmitted in real time without manual intervention. Thanks to that, banks can save on human resources costs and reduce workload.

- Build a unified customer data warehouse: Instead of storing individual information at each branch, eKYC allows customer data to be digitized and stored in a centralized CRM system, helping to manage customer data, cross-check information easily, and avoid duplication.

- Enhance security and safety: The eKYC process ensures that all transactions are performed by real customers, while continuously assessing and monitoring risks. Records and data are stored online, allowing for quick tracing of violations or abuses, contributing to increased customer confidence.

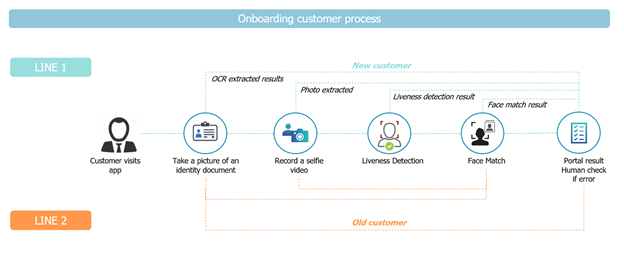

eKYC process when opening a payment account for an individual according to Vietnamese’s latest regulations

Based on Clause 1, Article 14a of Circular 23/2014/TT-NHNN, supplemented by Clause 6, Article 1 of Circular 16/2020/TT-NHNN on opening a payment account for an individual via electronic means:

When opening a payment account electronically, a bank or foreign bank branch is responsible for developing, promulgating and publicizing the process and procedures for opening a payment account. This process must comply with the provisions of Article 14a above, the provisions of law on anti-money laundering, electronic transactions, and at the same time ensure the safety and confidentiality of customer information and the safety of operations of the bank or foreign bank branch.

The eKYC process for opening a personal payment account electronically includes at least the following steps:

- Collecting information about the profile of the customer who wants to open a payment account as prescribed in Clause 1, Clause 4, Clause 5, Article 12 and Clause 1, Article 13 of this Circular.

- Comparing and verifying information to accurately identify the customer.

- Notifying prohibited or unauthorized acts during the process of opening and using a payment account opened electronically.

- Providing the content of the agreement to open and use a payment account as prescribed in Clause 1, Article 13a of this Circular, and at the same time signing the agreement with the customer.

- After completion, the bank must send a notice to the customer about the account number, account name, transaction limit on the same day the account starts operating.

What is the leading eKYC solution for businesses?

Since the beginning of July 2020, the State Bank has allowed about 10 banks to pilot eKYC. After only 2 months of VPBank launching the eKYC solution developed by FPT.AI, the bank has had more than 15,000 newly registered accounts, using 50% of the expected new accounts opened for the whole year of 2020.

Thanks to FPT AI eKYC, VPBank customers can verify their faces, biometrics, identity documents and some other documents that can authenticate their identity such as electricity and water bills (verifying address) or labor contracts (determining salary, place of work, etc.). This solution specifically requires the following types of documents:

- ID card/CCCD or Passport: Has clear information, clear portrait image, has a stamp to ensure that the documents are genuine and still valid.

- Household registration or temporary residence registration, Labor contract, Salary statement: Required when customers need to open a credit account, consumer loan, etc.). Customers must fulfill all requirements to use the service.

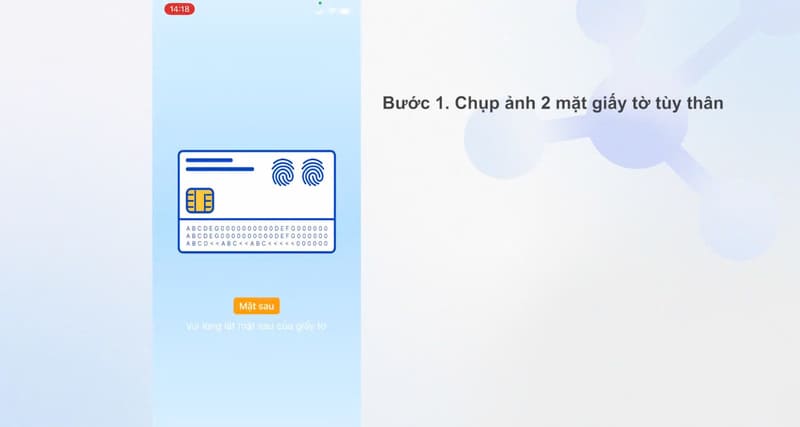

The identification process on FPT AI eKYC is as follows:

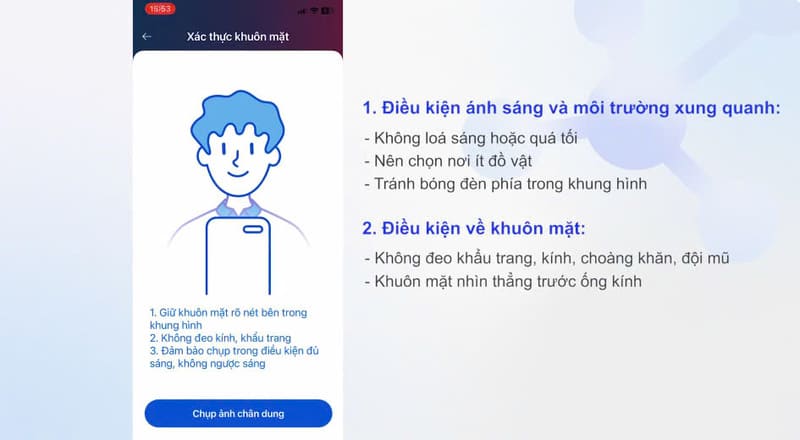

- Take a photo of your ID card: Users need to take a photo of both sides of their ID card, such as Citizen Identification Card (ID/CCCD), Driver’s License, Passport, etc. When taking a photo, place the document within the capture area on the screen, keep the document steady, and avoid glare or blurriness to ensure the image is clear, without losing corners or obscuring information.

- NFC Scan (Applicable to chip-based ID cards): If using a chip-based ID card, the customer needs to hold the ID card steady in the NFC scanning position on the phone. The system will read the data on the chip and authenticate the information on the ID card with data from the national database. When the scan is complete, the screen will display the message “Card reading completed”.

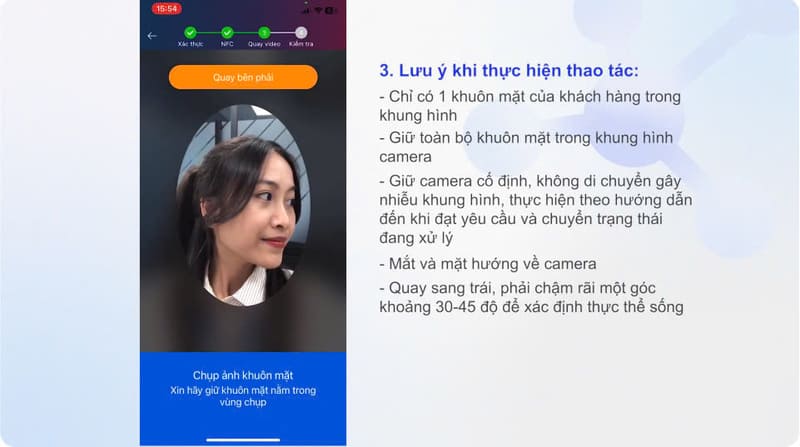

- Face Authentication (Liveness Detection): Customers take a photo of their face to verify their identity. When doing this, they need to look straight into the camera, turn their head slightly to the left and right (30-45 degrees), make sure their face is clearly in the frame, and do not wear glasses, masks, hats or other face coverings. In addition, make sure the lighting is adequate, not too dark or too bright. The system will match the face taken with the photo on the ID card, ensuring that the person taking the photo is a real person, not a photo or a replayed video.

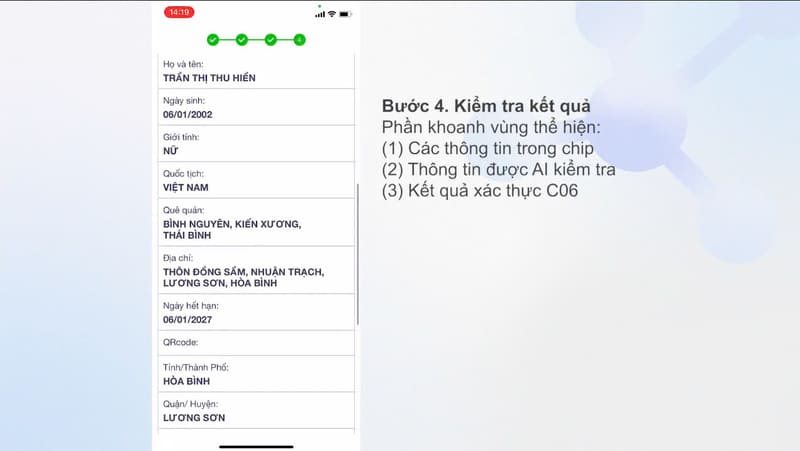

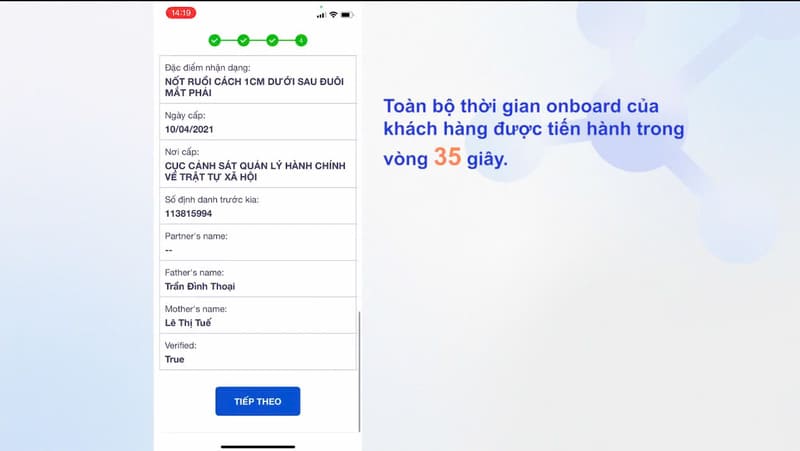

- Check and compare information: The system will display the authentication results including: Information on documents (full name, date of birth, gender, nationality, address, identification features, date of issue, place of issue), Information extracted from the chip (for chip-embedded CCCD), Biometric authentication results (Face Match, Liveness Check). If the information matches, the user selects “Next” to complete the eKYC process.

- Complete the eKYC process: Once all information is successfully verified, customers can continue to complete the account registration steps or use the service. The average time to complete the eKYC process is only about 35 seconds.

Recently, FPT AI eKYC has made an important mark in the electronic customer identification technology industry when it officially achieved ISO/IEC 30107-3 certification. This is a prestigious international standard, confirming the ability to detect and prevent the most sophisticated forms of forgery such as using still images, replay videos, or facial simulation tools. This achievement confirms that FPT AI eKYC has passed the Presentation Attack Detection (PAD) test of iBeta – a member of the FIDO Association and the world’s leading technology testing unit.

Integrating Generative AI, Face-Matching, Liveness Detection and Fraud Check, FPT AI eKYC not only promptly detects fake attacks but also reduces customer identification time by up to 70%, averaging only 35-40 seconds to complete a process with an accuracy of up to 98%.

ISO/IEC 30107-3 certification not only marks a major technological step forward but also demonstrates FPT Smart Cloud’s commitment to providing leading information security solutions, effectively serving leading financial, banking and securities organizations in Vietnam. The continuous innovation of FPT AI eKYC ensures optimal experience and absolute peace of mind for millions of customers, contributing to promoting the digital transformation trend in the financial sector.

Other frequently asked questions about eKYC

What are required conditions for banks to deploy eKYC technology in opening personal payment accounts electronically in Vietnam?

According to Clause 2, Article 14a of Circular 23/2014/TT-NHNN, supplemented by Clause 6, Article 1 of Circular 16/2020/TT-NHNN, banks or foreign bank branches are allowed to apply eKYC when meeting the following requirements:

(1) Having appropriate technology and measures to collect, check, compare and ensure the correct match between the customer’s identification information, biometric data and information on identification documents (stipulated in Clause 1, Article 12 of this Circular) or personal identification data authenticated by a competent state agency, or verified by another credit institution or an organization providing electronic identification and authentication services.

Among them, biometric data are biological characteristics that are difficult to fake and have a low duplication rate, such as fingerprints, faces, irises, voices, and other biometric factors.

(2) Have a technical solution to confirm that the customer, after being identified, has accepted the content of the agreement to open and use a payment account.

(3) Develop a risk management and assessment process, and take measures to prevent impersonation, interference, editing, and falsification of customer identification information before, during, and after opening an account. At the same time, have measures to check and verify to ensure that the person transacting on the electronic account is the account owner.

If risks, discrepancies, or unusual transactions related to customer identification information, or suspicious transactions (according to anti-money laundering laws and regulations), the bank must promptly refuse or stop the transaction, temporarily lock or freeze the account, and re-verify the information.

The risk management and control process needs to be reviewed and improved regularly based on information and data updated during the service provision process.

(4) Store all customer identification information, biometric data, audio, video, audio recordings, transaction phone numbers, and transaction logs in a complete, detailed, and timely manner.

Information and data must be kept safe, secure, and backed up to ensure completeness and integrity for inspection, comparison, settlement of inquiries, complaints, and disputes, and provided to competent state management agencies upon request. The storage period shall comply with the provisions of the law on anti-money laundering.

Does opening a payment account using eKYC apply to joint accounts and foreigners?

Pursuant to Clause 2, Article 14a of Circular 23/2014/TT-NHNN, supplemented by Clause 6, Article 1 of Circular 16/2020/TT-NHNN:

“Opening a payment account by electronic means as prescribed in this Article does not apply to joint payment accounts, individual customers who are foreigners and subjects specified in Points b, c, d, Clause 1, Article 11 of this Circular.”

Thus, opening a payment account by electronic means does not apply to joint payment accounts, individual customers who are foreigners and a number of other subjects specifically specified in Points b, c, d, Clause 1, Article 11 of Circular 23/2014/TT-NHNN (amended and supplemented).

———————————-

? Experience other products of #FPT_AI at: https://fpt.ai/vi

? Address: 7th Floor, FPT Tower, No. 10 Pham Van Bach, Cau Giay District, Hanoi

☎Hotline: 1900 638 399

? Email: support@fpt.ai

Reference source: Law Library. (n.d.). What is eKYC? Are banks allowed to deploy eKYC technology in opening personal payment accounts? Accessed on January 19, 2025, from

https://thuvienphapluat.vn/phap-luat/ekyc-la-gi-ngan-hang-duoc-phep-trien-khai-cong-nghe-ekyc-trong-mo-tai-khoan-thanh-toan-cua-ca-nhan–423989-151667.html